Cost Estimation and the Budget Baseline

The Number in the Charter Was Never the Budget

When the RtR project was approved, the charter authorized $368,000 for the full office relocation. That number was an early authorization estimate, not the cost baseline. It was built before the scope was defined, before activities were identified, and before a single resource was assigned: a rough order-of-magnitude figure that got the project approved. Now the job is to replace that early estimate with something defensible. Cost planning is the process that turns an authorization number into a grounded budget built from actual scope, actual resources, and actual rates.

Cost and Duration Are Not the Same Calculation

When you estimated duration, you were counting calendar days: how long will this take? Cost estimation requires a different lens entirely. Duration measures time. Cost measures money spent. The same activity can carry very different costs depending on who performs it. A senior specialist and a junior analyst might both take four days to complete a task. Their cost to the project is not the same. Labor hours multiplied by resource rates, materials purchased, equipment rented, and contractors engaged: these are cost inputs, not schedule inputs. The schedule tells you when costs occur. It does not tell you how much those costs are. Duration and cost must be estimated separately, even when they are closely related.

What a Cost Estimate Covers

A complete cost estimate accounts for every expenditure the project requires. Direct costs are the most visible: labor, materials, equipment, and external vendors. Indirect costs are less obvious but equally real, including facility use, administrative overhead, shared software licenses, and organizational services the project draws on. Some organizations track indirect costs with precision; others absorb them into a standard overhead rate. Know how your organization handles this before you begin. Missing a cost category does not make the cost disappear. It surfaces instead as a surprise during execution, when the budget conversation is harder to have.

Analogous Estimating: The Fast Read

Analogous estimating references a completed project of similar type and scale, then adjusts based on scope differences. It is fast and works well when information is limited. The RtR charter estimate of $368,000 is itself an analogous estimate: it was derived from what a previous office relocation had cost, adjusted for the differences in size and location. If that prior relocation cost $320,000 for a 38-person office and RtR is moving 45 people to a slightly larger space, scaling the reference figure up to $368,000 is a defensible starting point at the charter stage. It is not appropriate when a detailed WBS is in hand and real quotes are available. Analogous estimating works best early in planning, before the scope is fully defined, as a sanity check or initial authorization number.

Parametric Estimating: Unit Rate Applied to Quantity

Parametric estimating applies a unit rate to a known quantity: cost per square foot, cost per licensed user, cost per workstation setup. If historical data shows that office workstation procurement and setup runs $1,200 per station, and the new space needs 55 workstations, the parametric estimate for that work package is $66,000. No quote required once the rate and quantity are established. When reliable unit rates exist, either from past projects or industry benchmarks, parametric estimating is fast, transparent, and easy to challenge if the assumptions change.

The RtR security installation shows the difference between an analogous estimate and a grounded vendor quote. The charter used $64,000, drawn from a rough comparable on a previous project. When the team requested a formal quote based on the actual building specifications, floor plan, and access point counts, the contract came back at $135,000. The analogous figure was not replaced early enough. The $71,000 gap was always there. Planning just made it visible.

Bottom-Up Estimating: Building from the Work Package Up

Bottom-up estimating starts at the work package level. For each work package, the team estimates the labor hours required, identifies the resource who will do the work, applies their rate, and adds direct costs for materials and equipment. Each work package estimate then rolls up through the WBS levels to produce the project total. This is the most time-intensive technique, and the most defensible when the WBS is detailed and the input data is reliable. For the RtR project, this meant estimating the ITS contracting scope separately from the moving company, the real estate consulting fees separately from the cleaning service, and each materials line separately. The result is a number you can justify line by line because you built it that way.

Three-Point Estimating: Accounting for Uncertainty

When an estimate carries significant uncertainty, three-point estimating gives a single figure a more honest foundation. Instead of one number, you collect three: an optimistic estimate if everything goes smoothly, a most likely estimate under normal conditions, and a pessimistic estimate if significant problems arise. The PERT formula weights the most likely scenario most heavily.

For the RtR moving company work package: the team estimates an optimistic cost of $9,000 (a clean move with no complications), a most likely cost of $12,000 (normal conditions), and a pessimistic cost of $21,000 (delays, damage, or extra crew needed). The PERT estimate is ($9,000 + $48,000 + $21,000) divided by 6, which equals $13,000. That single number reflects the full range of scenarios rather than just the most optimistic outcome the team is privately hoping for. Three-point estimating does not eliminate uncertainty. It forces the team to acknowledge the range before committing to a number.

Documenting What the Estimate Assumes

A cost estimate is not just a number. It is a set of assumptions made visible. The basis of estimates records what you included, what you excluded, the source of each rate, and the confidence level of each figure. This documentation matters more than it seems at the time you write it. When a cost variance surfaces later, the first question is always: what did the estimate assume? If you documented it, you can answer clearly. If you did not, you are defending yourself from memory against a number that made sense six months ago for reasons no one can now reconstruct.

When the Planning Estimate Does Not Match the Charter

The planning estimate will often diverge from the charter budget. That gap is expected, because the charter number was built before a plan existed. Your planning estimate is grounded in real scope, real resources, and real rates. If there is a significant gap, that is a governance conversation, not a reason to quietly compress your numbers until they fit a figure that was never meant to be accurate. The RtR security installation gap is exactly this situation: the planning estimate produced a $71,000 increase on a single line item. Surface the variance early, with documentation, and let the sponsor respond to facts. Absorbing the difference silently leaves the project underfunded and sets up a harder conversation later, when there is less time to act on it.

Cost Aggregation: Rolling Up the WBS

Cost aggregation is the process of combining individual work package estimates into a project total. You start at the lowest level of the WBS and roll upward through deliverables to the full project cost. Many organizations also aggregate costs by spending category: labor, materials, contracted services, and equipment. This view is useful during execution because different categories behave differently across the project timeline. Labor costs tend to track with schedule progress. Material costs can spike when major procurements hit. Contracted services often front-load early in scope, then tail off. Aggregating by category gives better visibility into where money is actually going, and makes it easier to identify which category is driving a variance when one appears.

Reserve Structure: Two Buckets, Two Purposes

A cost estimate reflects the planned cost of the work. It does not cover every risk the project carries. Reserve analysis adds two layers of budget above the aggregated estimate, each with a distinct trigger and a different approval level.

The contingency reserve covers risks you have already identified. It is calculated from the risk register: probability multiplied by cost impact, summed across the known risks. The project manager controls this reserve within the authority limits defined in the cost management plan. You do not need executive approval to draw on it when a registered risk occurs, but you do need to document the risk event, the amount drawn, and the remaining balance. The contingency reserve is not a general buffer. It is assigned money with a specific purpose.

The management reserve covers what could not have been anticipated at all: budget for unknown unknowns, events so unexpected they were never registered as risks. The management reserve is not under the project manager's control. Accessing it requires a formal request and executive approval. Organizations typically set it as a percentage of the total budget, calibrated to the project's complexity and strategic importance. It is not a way to add new scope; it protects the approved project from unforeseeable cost impact within that scope. The table below captures the key distinctions between the two reserves.

| Contingency Reserve | Management Reserve | |

|---|---|---|

| Covers | Identified risks from the risk register | Unforeseeable events not in the risk register |

| Who controls it | Project Manager (within authority limits) | Executive / Sponsor |

| Access process | PM decision, documented draw | Formal request and executive approval |

| In cost baseline? | Yes | No |

| How calculated | Sum of P × I for each registered risk | Percentage of total budget (set by organization) |

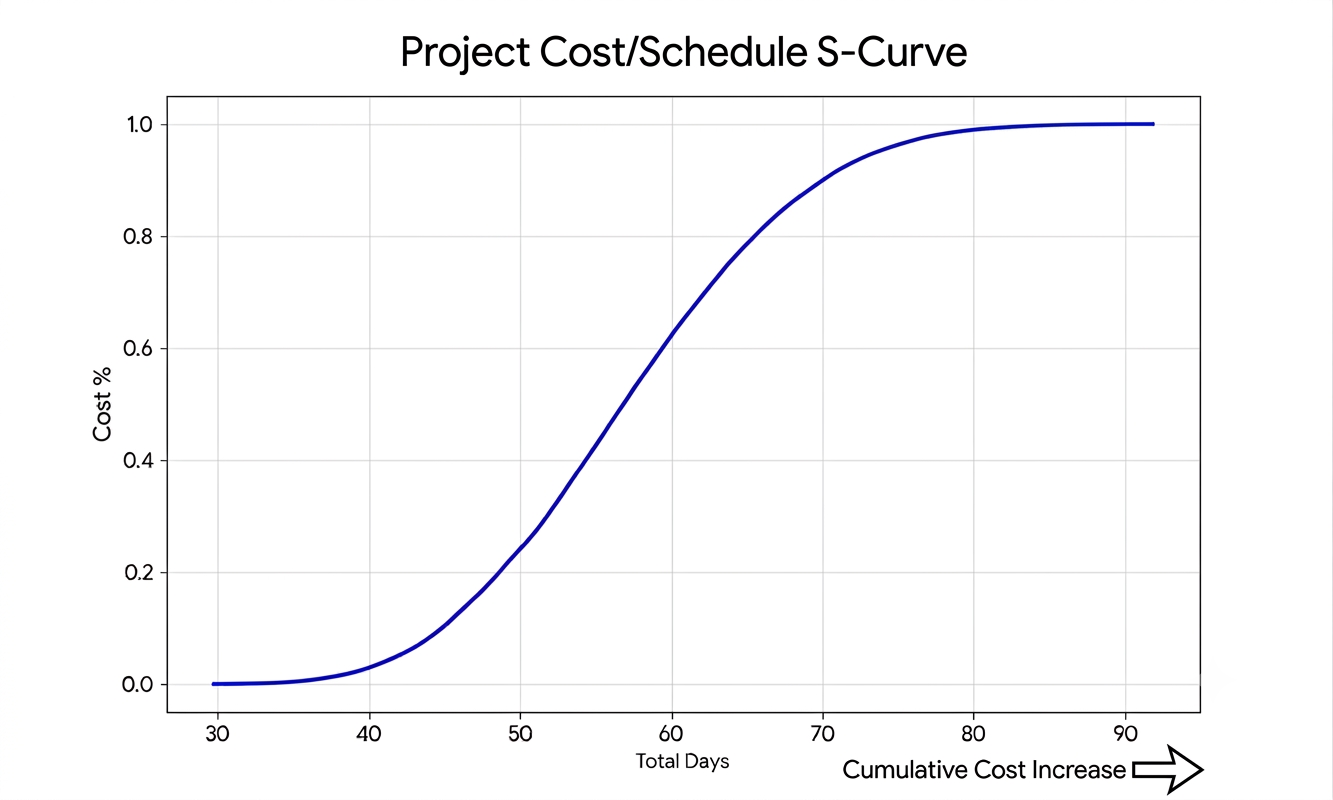

Time-Phasing and the S-Curve

A budget is not just a total. It is a total spread across time. That time-phasing is what makes the budget usable during execution. Early in a project, spending is low: planning activities, core team time, initial groundwork. As execution accelerates, spending picks up sharply, with resources fully deployed, materials ordered, and contractors engaged. Then it tapers as the project approaches completion. Plot cumulative spending over the project timeline and the curve forms a stretched letter S. That S-curve is the financial heartbeat of the project, the pattern against which actual spending is measured week by week. Without time-phasing, you cannot answer the question that matters during execution: are we spending at the rate the plan expected at this point in time?

What the Baseline Is and What It Does Not Include

The cost baseline is the approved, time-phased version of the project budget: the financial yardstick against which actual cost performance is measured throughout execution. It includes the aggregated work package estimates and the contingency reserve. It does not include the management reserve, which sits outside the project manager's span of control. The total funding requirement for the project, which the organization holds in reserve above the baseline, adds management reserve on top. The project manager is measured against the cost baseline, not against total funding held by the organization.

Once the baseline is approved, any change to it requires formal change control, not informal adjustments because a number looks inconvenient. Forecasts can and should be updated as reality changes; the approved baseline changes only when a formal scope or cost change is authorized. The baseline is a commitment, not a rough guide.

Why Baseline Discipline Matters

The cost baseline is only useful if it is protected. Once approved, it becomes the reference point for every cost conversation that follows: are we on track, ahead of plan, or over budget? Changing the baseline without formal approval quietly destroys that reference. You are no longer tracking performance against a plan. You are moving the target to wherever you currently are. This is a common way that cost overruns grow invisibly until they become crises. Protecting the baseline is not bureaucratic stubbornness. It is how you maintain an honest picture of project health, for yourself and for every stakeholder who relies on the status you report.

Thesis Yu's job after charter approval was to replace the $368,000 authorization with a grounded baseline. The first step was requesting formal quotes rather than carrying forward analogous figures. The security installation quote came in at $135,000 against a charter estimate of $64,000. That $71,000 gap went directly to Padre Moneyholder with clear framing: this is what the project now knows, and here are the options. Absorbing it silently into contingency was not an option, because that would have immediately consumed the reserve before a single risk event occurred.

One area remained unresolved: renovations. The new space required a physical assessment before any renovation estimate could be reliable. Thesis recorded this honestly as a question mark in the budget, not a placeholder number. A manufactured figure would have given the baseline a false sense of completeness and created a reconciliation problem when the real cost arrived.

The confirmed estimate for known scope stood at $248,075, with renovations still unresolved. A full cost baseline cannot be approved until renovations are estimated or an explicit allowance is authorized. Thesis presented this honestly: here are the costs we can confirm, here is the open item, and here is the decision the sponsor needs to make before the baseline can close.

| Cost Category | Line Item | Amount |

|---|---|---|

| Contracted Services | Real Estate Consulting Services | $18,000 |

| ITS Contracting | $42,000 | |

| Security Installation Contract | $135,000 | |

| Moving Company | $12,500 | |

| Cleaning Service | $1,200 | |

| Contracted Services Subtotal | $208,700 | |

| Materials | Network Cabling and Technology Room | $8,200 |

| Dispatch Temporary Workstations | $4,500 | |

| Moving Boxes | $325 | |

| Opening Day Celebration | $850 | |

| Materials Subtotal | $13,875 | |

| Renovations | Pending physical assessment | TBD |

| Contingency Reserve | Identified risks from risk register | $25,500 |

| Confirmed Estimate (Renovations Pending) | $248,075 + TBD | |

Charter authorization: $368,000. Confirmed estimate for known scope: $248,075. Renovations: open. The security gap and the renovation unknowns each need a decision: find savings elsewhere, request a budget amendment, or reduce scope. The estimate does not make those decisions. It makes them possible to have.

Three days after the cost baseline was approved, three team members hand in their resignations. A competitor announced a new location nearby and moved quickly to staff up. The three people who left held specialized skills factored directly into the resource plan, the schedule, and the estimates. The budget everyone signed off on assumed this team. That team no longer exists.

Replacing these roles with contract staff is not a one-to-one swap. Contract rates for the skill set run higher than the original internal resource costs, significantly higher given that the competitor's arrival has tightened the local talent pool. The early estimate for replacement comes in at roughly forty percent above the original labor cost for those three roles. Add two to three weeks of onboarding before the replacements reach full productivity, and the schedule impact starts cascading. The contingency reserve would cover this. The math fits. But the contingency reserve was built from the risk register, probability times cost impact, risk by risk. Each dollar in that reserve is assigned to a specific identified risk. A talent drain triggered by a competitor that was not on the map when the register was built is not one of those risks. Using the contingency reserve here would cover today's problem and leave every registered risk exposed. If any of those risks materialize later, the reserve will be gone and there will be no answer.

The management reserve was established for exactly this situation: an unforeseen event that falls outside the risk register entirely. Accessing it requires a formal request and executive approval. That conversation will not be easy. The sponsor signed off on a budget three days ago based on a specific team. But the alternative is drawing on funds earmarked for registered risks, which creates two problems instead of one.

The cost impact document is built before the meeting is requested. Replacement labor cost versus the original estimate, line by line. Onboarding timeline and its effect on the schedule. Three scenarios: access the management reserve as the reserve structure intended, reduce scope to absorb the cost within the existing baseline, or extend the timeline and revisit at the next governance checkpoint. The PM is not walking in to apologize. The PM is walking in with a structured analysis and a set of choices. When the formal request is made and the impact presented clearly, the baseline stays intact, the contingency reserve remains available for the risks it was assigned to, and the project has a defensible path forward. That is what reserve structure is for: not just to have a number, but to have a system that holds when the project meets something it did not expect.

The Third Leg of the Triple Constraint

The schedule baseline locked the project's time commitment. The scope statement locked what the project will deliver. The cost baseline, once approved, completes the triple constraint: the three-sided boundary within which the project is authorized to operate. Each one was built in sequence, scope first, then schedule, then cost, because each one depends on what came before. Each one is locked for the same reason: so there is a plan to measure against. With all three baselines in place, execution can begin with a clear reference point for every decision that follows.

What's Next

With scope, schedule, and cost baselines established, planning shifts to quality. Quality planning defines what "done" looks like beyond simply completing activities on time and within budget. It sets the standards the deliverables must meet, the methods for verifying that they meet those standards, and the approach to preventing defects before they occur rather than catching them afterward. Quality Planning is the next chapter.

Reflect

- Where in your current project did the original budget authorization come from, and what assumptions was it based on? How closely does it match what a bottom-up estimate would produce?

- What would change about how your team builds cost estimates if you were required to document the basis of estimates, including sources and confidence levels, for every line item?

- How does your team currently handle the difference between the contingency reserve and the management reserve? Are they treated as separate buckets with distinct triggers, or as a single pool?

- When was the last time your project's planning-phase estimate diverged significantly from the charter budget? How was that gap communicated to the sponsor, and what decision came out of that conversation?

- What would a colleague observing your last project's budget baseline say about whether it was protected as a fixed reference point, or quietly adjusted to match actual spending as the project progressed?

Agile Project Management & Scrum — With AI

Ship value sooner, cut busywork, and lead with confidence. Whether you’re new to Agile or scaling multiple teams, this course gives you a practical system to plan smarter, execute faster, and keep stakeholders aligned.

This isn’t theory—it’s a hands-on playbook for modern delivery. You’ll master Scrum roles, events, and artifacts; turn vision into a living roadmap; and use AI to refine backlogs, write clear user stories and acceptance criteria, forecast with velocity, and automate status updates and reports.

You’ll learn estimation, capacity and release planning, quality and risk management (including risk burndown), and Agile-friendly EVM—plus how to scale with Scrum of Scrums, LeSS, SAFe, and more. Downloadable templates and ready-to-use GPT prompts help you apply everything immediately.

Learn proven patterns from real projects and adopt workflows that reduce meetings, improve visibility, and boost throughput. Ready to level up your delivery and lead in the AI era? Enroll now and start building smarter sprints.

Lead with clarity, influence, and outcomes.

HK School of Management brings you a practical, no-fluff Leadership for Project Managers course—built for real projects, tight deadlines, and cross-functional teams. Learn to set direction, align stakeholders, and drive commitment without relying on title. For the price of a lunch, get proven playbooks, and downloadable templates. Backed by a 30-day money-back guarantee—zero risk, high impact.

Learn More